1")

2")

3")

4")

5")

6")

7")

8")

9")

10")

12")

13")

Indexes: Nifty | Bank Nifty | Finnifty | Midcap Nifty | Sensex | Bankex

Are you doing Stockmock backtesting and want to automate your strategies?

Telegram channel: https://t.me/myalgomatestraddle Or search “myalgomatestraddle” in TG.

You can configure your strategy to enter at a specific time of the day.

For example, if you want the strategy to take entry at 09:25 AM, simply set the desired entry time.

Trigger entry when the Live Market Price (LTP) of your selected underlying (e.g., Nifty spot, Futures, or Synthetic Futures) crosses a certain threshold.

Example:

Frequency Options:

You can choose how frequently the system should check this condition:

Start Time Validation:

The system will not evaluate the condition before the specified Start Time.

Example: If Start Time = 09:30:00, the condition will only be checked on or after 09:30 AM.

Trigger entry based on the ATM (At-the-Money) Straddle Premium.

Example:

How It Works:

Frequency Options:

Just like price-based conditions, you can choose:

Start Time Validation:

The system will not evaluate the condition before the specified Start Time.

Example: If Start Time = 09:30:00, the condition will only be checked on or after 09:30 AM.

Specific Days of the Week

You can manually choose the weekdays on which the strategy should be active.

For example: Run only on Monday, Wednesday, and Friday

Days from Expiry

Alternatively, you can set the strategy to run based on the number of days remaining to expiry of the underlying instrument.

Example:

Run the strategy only on 2 days before expiry (e.g., Tuesday for a Thursday expiry)

Decide which trading accounts the strategy should execute on.

Individual Account Selection

Manually pick one or more accounts on which the strategy should run.

Account Groups

You can create groups of accounts (e.g.,10L Fund, 50L Fund) and then choose an entire group for strategy execution.

Select the option strike based on their distance from the ATM strike in terms of strike steps.

How it works:

Example:

Note:

If the input value is invalid or too far (e.g., the strike doesn’t exist), the system will skip the entry and show an error: “Contract not found.”

Select option strikes based on a percentage distance from the ATM price.

How it works:

Example:

Let’s say BankNifty’s ATM is at 45000.

Note:

If the calculated strike doesn’t exist, the system will not take entry and will show an error: “Contract not found.”

This method allows you to manually enter the exact strike price you want to use for a leg. If you want to trade the 45200 CE, then enter 45200 in the strike input.

Note:

If the contract does not exist (e.g., expired or incorrect strike), the system will not place the order and will show an error:

“Contract not found.”

This method selects option contracts based on the delta value closest to your target, using the same match logic as the premium-based method.

How it works:

You need to specify:

Example:

Delta Match Options

If no contract is found within the specified match range, choose one of the following:

Important Notes:

This method allows you to select CE/PE (CP) legs based on the combined premium (SP) of the ATM straddle. It is useful when you want to define strikes relative to the current premium structure.

How it works:

Example:

Supported Comparison Operators:

Note:

This method selects the option contract based on the width of the ATM straddle premium. It calculates a revised strike by multiplying the ATM straddle price by a user-defined width factor, adds it to the ATM strike, and rounds the result to the nearest valid strike.

How it works:

So it will select 46000 CE.

Wait and Trade (W&T) allows you to delay execution until the price of the option or the underlying moves by a defined value from its trigger-time price.

You can configure W&T separately for Options and Underlying with different input types.

Option W&T Inputs

When W&T is enabled for option contracts, the system records the option premium at the moment the entry condition is met, and waits for the price to move based on the selected input.

Available Inputs:

Examples:

Underlying W&T Inputs

When W&T is enabled for the underlying, the system records the underlying price (Spot/Future/Synthetic) at the moment of strategy trigger and waits for the price to move as configured.

Available Inputs:

Examples:

Note:

For option price-based W&T only, you can choose whether to pre-place the W&T order on the broker terminal using the “Place W&T Order in Broker” checkbox available in the order settings.

The Trail Wait & Trade (W&T) feature introduces a more dynamic and adaptive approach to trade executions, ensuring your entries are always in sync with evolving market movements.

How It Works

Instead of fixing your wait price at a set distance from the trigger level, Trail W&T dynamically adjusts the wait price in your favor as the underlying price moves further from your original trigger. If the market continues to move away from your trigger, the wait price trails along—ensuring your entry happens only on a meaningful pullback, and at the best possible level.

Example: Wait Above (Upside)

Example: Wait Below (Downside)

Applicability

Trail W&T applies to both option-based and underlying-based Wait & Trade. Additionally, if you have enabled Wait & Trade for re-entry or re-execute conditions, Trail W&T is applicable for those scenarios as well, providing consistent, intelligent entry handling throughout all stages of your strategy.

Enabling Trail W&T

You can enable Trail Wait & Trade by checking the “Enable Trail Wait & Trade” option in the Other Settings section while creating your strategy.

The Target setting allows you to define the exit condition for each leg individually, based on either the option premium or the underlying price reaching a specific target.

You can choose one of the following target types per leg:

Target on Option Price

Available Inputs:

Examples:

Target on the Underlying Price

Available Inputs:

Direction of Target Exit based on Position Type:

Examples:

Note:

In the Other Settings section, using the SL/Target base configuration selection, you can configure whether the target price should be calculated based on the actual traded price (order execution price) or LTP at the time of entry. This setting is applicable only for option-based targets.

For underlying-based targets, the system always uses the underlying price at the time of entry to calculate target levels.

The Stoploss setting allows you to define the exit condition for each leg individually, based on either the option premium or the underlying price reaching a specific stop level.

You can choose one of the following stop-loss types per leg:

Stop Loss on Option Price

Available Inputs:

Examples:

Stoploss on the Underlying Price

Available Inputs:

Direction of Stoploss Exit based on Position Type:

Examples:

Note:

You can also configure whether or not to place the stoploss order in the broker terminal using the checkbox “Place SL in Broker” in the order settings. This is applicable for Option Option-based SL only. Underlying SL can’t be placed in the broker.

Trailing can be configured for Option SL and Underlying SL.

You can set Trail X and Trail Y in either percentage or points.

Example: Option SL – Buy Leg (X and Y in %)

Entry Type: Buy

Entry Price: 100

Initial SL %: 10% → SL = 90

Trailing X% = 5%, Trailing Y% = 5%

Calculation:

Trail Steps:

Example: Option SL – Sell Leg (X and Y in Points)

Entry Type: Sell

Entry Price: 100

Initial SL: 10 points → SL = 110

Trailing X: 5 points

Trailing Y: 5 points

Calculation:

Trail Steps:

Example: Underlying SL – CE Sell Leg (X and Y in %)

Leg Type: CE

Entry Type: Sell

Underlying at Entry: 45000

Initial SL: 0.1% → SL = 45045

Trailing X: 0.1%

Trailing Y: 0.1%

Calculation:

Trail Steps:

Example: Underlying SL – PE Sell Leg (X and Y in Points)

Leg Type: PE

Entry Type: Sell

Underlying at Entry: 45000

Initial SL: 100 points → SL = 44900

Trailing X: 20 points

Trailing Y: 20 points

Calculation:

Trail Steps:

Note:

For underlying-based SL, trailing happens internally and is not pushed to the broker.

The Re-Entry @ Cost feature allows the system to take a fresh position in the same contract after a stoploss exit, if the price returns back to the original entry price.

After hitting the stoploss, the system monitors whether the price comes back to the entry level:

Re-Entry Types

You can configure how the re-entry condition is checked:

Examples

Example 1: Option SL with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option SL with LTP Basis (Buy Entry)

Flow:

Example 3: Underlying SL with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying SL with LTP Basis (Call Buy Entry)

Flow:

Other Configurable Parameters

Stop Re-Entry Time

Number of Re-Entries

Wait for Original SL Price

Disable Re-Entry if SL moved to Cost

Disable Re-Entry if Trail SL crossed Cost

W&T with Re-Entry @ Cost

The Re-Execute on SL feature allows the system to open a new position after the stoploss is hit. Unlike Re-Entry @ Cost, which waits for the price to return to the original entry price, Re-Execute triggers a fresh entry directly after SL hit, based on user configuration.

In Re-Execute, the system always selects a new contract as per the active contract selection method when re-execute triggers.

How Re-Execute Works

After the stoploss is hit:

Re-Execute Types

Examples

Example 1: Option SL with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option SL with Immediate Re-Execute (Buy Entry)

Flow:

Example 3: Underlying SL with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying SL with Immediate Re-Execute (Call Buy Entry)

Flow:

Key Differences Between Re-Entry @ Cost and Re-Execute on SL

| Feature | Re-Entry @ Cost | Re-Execute on SL |

| Entry Condition | Waits for price to return to original entry price | Triggers after SL hit based on immediate or candle close setting |

| Contract Selection | Same contract as original | New contract selected as per contract selection method |

| Timing | LTP basis or Candle Closing basis | Immediate or Candle Closing basis |

The Re-Execute Reverse feature works similarly to Re-Execute on SL, but with one key difference:

It alternates the direction of each re-execute after a stoploss is hit.

How Re-Execute Reverse Works

Behavior Summary

| SL Hit Count | Action Type (for initial Sell entry) |

| 1st Entry | Sell |

| After 1st SL | Buy |

| After 2nd SL | Sell |

| After 3rd SL | Buy |

| And so on… | Alternates each time |

Key Differences Between Re-Execute and Re-Execute Reverse

| Feature | Re-Execute on SL | Re-Execute Reverse |

| Entry Direction | Same as original entry type on each re-execute | Alternates direction (Sell ↔ Buy) on each re-execute |

The Re-Entry @ Cost for Target feature allows the system to take a fresh position in the same contract after a target exit, if the price returns back to the original entry price.

After hitting the target, the system monitors whether the price comes back to the entry level:

Re-Entry Types

You can configure how the re-entry condition is checked:

Examples

Example 1: Option Target with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option Target with LTP Basis (Buy Entry)

Flow:

Example 3: Underlying Target with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying Target with LTP Basis (Call Buy Entry)

Flow:

Other Configurable Parameters

Stop Re-Entry Time

Number of Re-Entries

W&T with Re-Entry @ Cost

Note:

The following options are not applicable for Target-based Re-Entry:

The Re-Execute on Target feature allows the system to open a new position after the target is achieved. Unlike Re-Entry @ Cost, which waits for the price to return to the original entry price, Re-Execute triggers a fresh entry directly after the target is hit, based on user configuration.

In Re-Execute on Target, the system always selects a new contract as per the active contract selection method when re-execute triggers.

How Re-Execute Works

After the target is hit:

Re-Execute Types

Examples

Example 1: Option Target with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option Target with Immediate Re-Execute (Buy Entry)

Flow:

Example 3: Underlying Target with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying Target with Immediate Re-Execute (Call Buy Entry)

Flow:

Key Differences Between Re-Entry @ Cost and Re-Execute on Target

| Feature | Re-Entry @ Cost | Re-Execute on Target |

| Entry Condition | Waits for price to return to original entry price | Triggers after target hit based on immediate or candle close setting |

| Contract Selection | Same contract as original | New contract selected as per contract selection method |

| Timing | LTP basis or Candle Closing basis | Immediate or Candle Closing basis |

The Re-Execute Reverse for Target feature works similarly to Re-Execute on Target, but with one key difference:

It alternates the direction of each re-execute after a target is hit.

How Re-Execute Reverse Works

Behavior Summary

| Target Hit Count | Action Type (for initial Sell entry) |

| 1st Entry | Sell |

| After 1st Target | Buy |

| After 2nd Target | Sell |

| After 3rd Target | Buy |

| And so on… | Alternates each time |

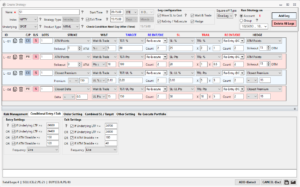

Hedge contracts can be configured for each strategy leg to reduce margin requirements or manage risk exposure. You can select the hedge contract in two ways:

In both methods, separate configuration is provided specifically for hedge contract selection, allowing independent control over how hedge contracts are chosen.

Additionally, there is a special option:

During exit, the system always exits the main leg first, and once completed, it exits the hedge leg.

Method 1: ATM Points Based Hedge Selection

This method selects the hedge contract based on its distance from the ATM strike in terms of strike steps.

How it works:

Example:

Note:

Method 2: Closest Premium Based Hedge Selection

This method selects the hedge contract whose premium is closest to your specified target premium using configurable match conditions.

How it works:

You need to specify:

Example:

Premium Match Options:

If no contract is found within the specified match range, you can configure the fallback behavior:

Note:

Hedge premium match uses a separate Hedge Match Settings section.

You can configure it with two options:

Example:

Example:

Parameters

Example:

Flow:

Note:

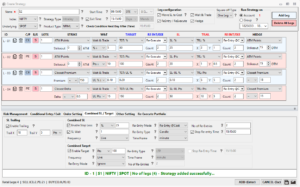

The Combined SL feature allows you to define a stoploss at the portfolio level based on the combined entry price of multiple legs.

Prerequisites:

How Combined SL Works:

Example:

Available Parameters for Combined SL:

Trailing SL: X and Y configurable in % or Points

Note:

Other advanced re-entry filters (Wait for Original SL, Disable Re-entry if SL moved to cost, etc.) are not applicable for Combined SL Re-Entry.

Re-Execute Types:

Configurable Parameters:

Stop Re-Execute Time

| Combined SL Hit Count | Entry Direction (assuming initial Sell) |

| 1st Entry | Sell |

| After 1st SL | Buy |

| After 2nd SL | Sell |

| After 3rd SL | Buy |

| … | Alternates each time |

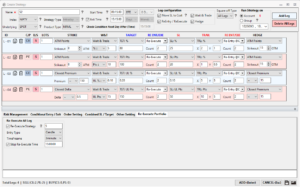

The Combined Target feature allows you to define a target at the portfolio level based on the combined entry price of multiple legs.

Prerequisites:

How Combined Target Works:

Example:

Available Parameters for Combined Target:

Note:

Other advanced re-entry filters (Wait for Original SL, Disable Re-entry if SL moved to cost, etc.) are not applicable for Combined Target Re-Entry.

Re-Execute Types:

Configurable Parameters:

Candle timeframe

Stop Re-Execute Time

| Combined Target Hit Count | Entry Direction (assuming initial Sell) |

| 1st Entry | Sell |

| After 1st Target | Buy |

| After 2nd Target | Sell |

| After 3rd Target | Buy |

| … | Alternates each time |

Order Settings allow you to control how orders are placed and managed for:

You can configure different settings for Entry Orders and Exit Orders independently.

Order Type

You can select:

Limit Price Configuration (Applicable for Limit Orders Only)

Limit Price Calculation Examples

Example 1 — LTP Reference

Example 2 — BestBidAsk Reference

Example 3 — ImFill Reference

Example 4 — AvgBidAsk Reference

Limit Order Revision Logic

If the limit order is not filled, the system can automatically modify it using the following two revision methods:

Option 1: Modify to Market

Option 2: Revise Limit Price

Separate settings apply for orders placed as Stoploss (SL) orders in broker.

Order Type for SL Orders

Trigger Price

Limit Price for SL Order

Limit Price Calculation Example

(For Buy orders, buffer is added to Trigger Price; for Sell orders, buffer is subtracted.)

SL Order Revision Logic (Same as Entry/Exit orders)

📸 [Screenshot showing SL Order Settings with Limit Buffer and Revision Logic]

Summary

| Configuration | Entry Orders | Exit Orders (Non-SL) | SL Orders |

| Market Order | Available | Available | Not Available |

| Limit Order | Available | Available | Always Limit |

| Limit Reference | Available | Available | Available |

| Limit Buffer | Available | Available | Available |

| Revision Logic | Available | Available | Available |

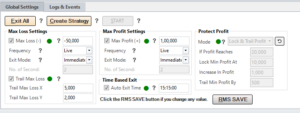

Max Loss defines the maximum allowed drawdown.

Example (Strategy Level):

For Account Level / Global Level:

Parameters for Max Loss:

Ticks Based:

Exit only if Max Loss condition holds true for X number of consecutive ticks.

Trail Max Loss allows you to dynamically tighten your Max Loss as profit increases.

Parameters:

Example:

Flow:

Same behavior applies for Account Level and Global Level — only MTM calculation changes as per level.

Max Profit defines the maximum profit at which you want to exit and book profits.

Parameters and behavior are exactly same as Max Loss:

Frequency to Check, Exit Mode, and Ticks Based logic all apply exactly as in Max Loss.

Protect Profit helps secure profits dynamically as your profit grows. Three modes are available:

Allows you to lock a fixed minimum profit once your profit crosses a threshold.

Parameters:

Example:

Flow:

Allows you to trail profits upward step-by-step as profits grow.

Parameters:

Example:

Flow:

Combines both Lock and Trail methods together.

Parameters:

Example:

Flow:

Applicable Behavior Across All Levels:

| Level | MTM Calculation |

| Strategy Level | MTM of individual strategy |

| Account Level | Total MTM across all strategies of that account |

| Global Level | Total MTM across all accounts |

You can configure your strategy to enter at a specific time of the day.

For example, if you want the strategy to take entry at 09:25 AM, simply set the desired entry time.

Trigger entry when the Live Market Price (LTP) of your selected underlying (e.g., Nifty spot, Futures, or Synthetic Futures) crosses a certain threshold.

Example:

Frequency Options:

You can choose how frequently the system should check this condition:

Start Time Validation:

The system will not evaluate the condition before the specified Start Time.

Example: If Start Time = 09:30:00, the condition will only be checked on or after 09:30 AM.

Trigger entry based on the ATM (At-the-Money) Straddle Premium.

Example:

How It Works:

Frequency Options:

Just like price-based conditions, you can choose:

Start Time Validation:

The system will not evaluate the condition before the specified Start Time.

Example: If Start Time = 09:30:00, the condition will only be checked on or after 09:30 AM.

Specific Days of the Week

You can manually choose the weekdays on which the strategy should be active.

For example: Run only on Monday, Wednesday, and Friday

Days from Expiry

Alternatively, you can set the strategy to run based on the number of days remaining to expiry of the underlying instrument.

Example:

Run the strategy only on 2 days before expiry (e.g., Tuesday for a Thursday expiry)

Decide which trading accounts the strategy should execute on.

Individual Account Selection

Manually pick one or more accounts on which the strategy should run.

Account Groups

You can create groups of accounts (e.g.,10L Fund, 50L Fund) and then choose an entire group for strategy execution.

Select the option strike based on their distance from the ATM strike in terms of strike steps.

How it works:

Example:

Note:

If the input value is invalid or too far (e.g., the strike doesn’t exist), the system will skip the entry and show an error: “Contract not found.”

Select option strikes based on a percentage distance from the ATM price.

How it works:

Example:

Let’s say BankNifty’s ATM is at 45000.

Note:

If the calculated strike doesn’t exist, the system will not take entry and will show an error: “Contract not found.”

This method allows you to manually enter the exact strike price you want to use for a leg. If you want to trade the 45200 CE, then enter 45200 in the strike input.

Note:

If the contract does not exist (e.g., expired or incorrect strike), the system will not place the order and will show an error:

“Contract not found.”

This method selects option contracts based on the delta value closest to your target, using the same match logic as the premium-based method.

How it works:

You need to specify:

Example:

Delta Match Options

If no contract is found within the specified match range, choose one of the following:

Important Notes:

This method allows you to select CE/PE (CP) legs based on the combined premium (SP) of the ATM straddle. It is useful when you want to define strikes relative to the current premium structure.

How it works:

Example:

Supported Comparison Operators:

Note:

This method selects the option contract based on the width of the ATM straddle premium. It calculates a revised strike by multiplying the ATM straddle price by a user-defined width factor, adds it to the ATM strike, and rounds the result to the nearest valid strike.

How it works:

So it will select 46000 CE.

Wait and Trade (W&T) allows you to delay execution until the price of the option or the underlying moves by a defined value from its trigger-time price.

You can configure W&T separately for Options and Underlying with different input types.

Option W&T Inputs

When W&T is enabled for option contracts, the system records the option premium at the moment the entry condition is met, and waits for the price to move based on the selected input.

Available Inputs:

Examples:

Underlying W&T Inputs

When W&T is enabled for the underlying, the system records the underlying price (Spot/Future/Synthetic) at the moment of strategy trigger and waits for the price to move as configured.

Available Inputs:

Examples:

Note:

For option price-based W&T only, you can choose whether to pre-place the W&T order on the broker terminal using the “Place W&T Order in Broker” checkbox available in the order settings.

The Trail Wait & Trade (W&T) feature introduces a more dynamic and adaptive approach to trade executions, ensuring your entries are always in sync with evolving market movements.

How It Works

Instead of fixing your wait price at a set distance from the trigger level, Trail W&T dynamically adjusts the wait price in your favor as the underlying price moves further from your original trigger. If the market continues to move away from your trigger, the wait price trails along—ensuring your entry happens only on a meaningful pullback, and at the best possible level.

Example: Wait Above (Upside)

Example: Wait Below (Downside)

Applicability

Trail W&T applies to both option-based and underlying-based Wait & Trade. Additionally, if you have enabled Wait & Trade for re-entry or re-execute conditions, Trail W&T is applicable for those scenarios as well, providing consistent, intelligent entry handling throughout all stages of your strategy.

Enabling Trail W&T

You can enable Trail Wait & Trade by checking the “Enable Trail Wait & Trade” option in the Other Settings section while creating your strategy.

The Target setting allows you to define the exit condition for each leg individually, based on either the option premium or the underlying price reaching a specific target.

You can choose one of the following target types per leg:

Target on Option Price

Available Inputs:

Examples:

Target on the Underlying Price

Available Inputs:

Direction of Target Exit based on Position Type:

Examples:

Note:

In the Other Settings section, using the SL/Target base configuration selection, you can configure whether the target price should be calculated based on the actual traded price (order execution price) or LTP at the time of entry. This setting is applicable only for option-based targets.

For underlying-based targets, the system always uses the underlying price at the time of entry to calculate target levels.

The Stoploss setting allows you to define the exit condition for each leg individually, based on either the option premium or the underlying price reaching a specific stop level.

You can choose one of the following stop-loss types per leg:

Stop Loss on Option Price

Available Inputs:

Examples:

Stoploss on the Underlying Price

Available Inputs:

Direction of Stoploss Exit based on Position Type:

Examples:

Note:

You can also configure whether or not to place the stoploss order in the broker terminal using the checkbox “Place SL in Broker” in the order settings. This is applicable for Option Option-based SL only. Underlying SL can’t be placed in the broker.

Trailing can be configured for Option SL and Underlying SL.

You can set Trail X and Trail Y in either percentage or points.

Example: Option SL – Buy Leg (X and Y in %)

Entry Type: Buy

Entry Price: 100

Initial SL %: 10% → SL = 90

Trailing X% = 5%, Trailing Y% = 5%

Calculation:

Trail Steps:

Example: Option SL – Sell Leg (X and Y in Points)

Entry Type: Sell

Entry Price: 100

Initial SL: 10 points → SL = 110

Trailing X: 5 points

Trailing Y: 5 points

Calculation:

Trail Steps:

Example: Underlying SL – CE Sell Leg (X and Y in %)

Leg Type: CE

Entry Type: Sell

Underlying at Entry: 45000

Initial SL: 0.1% → SL = 45045

Trailing X: 0.1%

Trailing Y: 0.1%

Calculation:

Trail Steps:

Example: Underlying SL – PE Sell Leg (X and Y in Points)

Leg Type: PE

Entry Type: Sell

Underlying at Entry: 45000

Initial SL: 100 points → SL = 44900

Trailing X: 20 points

Trailing Y: 20 points

Calculation:

Trail Steps:

Note:

For underlying-based SL, trailing happens internally and is not pushed to the broker.

The Re-Entry @ Cost feature allows the system to take a fresh position in the same contract after a stoploss exit, if the price returns back to the original entry price.

After hitting the stoploss, the system monitors whether the price comes back to the entry level:

Re-Entry Types

You can configure how the re-entry condition is checked:

Examples

Example 1: Option SL with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option SL with LTP Basis (Buy Entry)

Flow:

Example 3: Underlying SL with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying SL with LTP Basis (Call Buy Entry)

Flow:

Other Configurable Parameters

Stop Re-Entry Time

Number of Re-Entries

Wait for Original SL Price

Disable Re-Entry if SL moved to Cost

Disable Re-Entry if Trail SL crossed Cost

W&T with Re-Entry @ Cost

The Re-Execute on SL feature allows the system to open a new position after the stoploss is hit. Unlike Re-Entry @ Cost, which waits for the price to return to the original entry price, Re-Execute triggers a fresh entry directly after SL hit, based on user configuration.

In Re-Execute, the system always selects a new contract as per the active contract selection method when re-execute triggers.

How Re-Execute Works

After the stoploss is hit:

Re-Execute Types

Examples

Example 1: Option SL with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option SL with Immediate Re-Execute (Buy Entry)

Flow:

Example 3: Underlying SL with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying SL with Immediate Re-Execute (Call Buy Entry)

Flow:

Key Differences Between Re-Entry @ Cost and Re-Execute on SL

| Feature | Re-Entry @ Cost | Re-Execute on SL |

| Entry Condition | Waits for price to return to original entry price | Triggers after SL hit based on immediate or candle close setting |

| Contract Selection | Same contract as original | New contract selected as per contract selection method |

| Timing | LTP basis or Candle Closing basis | Immediate or Candle Closing basis |

The Re-Execute Reverse feature works similarly to Re-Execute on SL, but with one key difference:

It alternates the direction of each re-execute after a stoploss is hit.

How Re-Execute Reverse Works

Behavior Summary

| SL Hit Count | Action Type (for initial Sell entry) |

| 1st Entry | Sell |

| After 1st SL | Buy |

| After 2nd SL | Sell |

| After 3rd SL | Buy |

| And so on… | Alternates each time |

Key Differences Between Re-Execute and Re-Execute Reverse

| Feature | Re-Execute on SL | Re-Execute Reverse |

| Entry Direction | Same as original entry type on each re-execute | Alternates direction (Sell ↔ Buy) on each re-execute |

The Re-Entry @ Cost for Target feature allows the system to take a fresh position in the same contract after a target exit, if the price returns back to the original entry price.

After hitting the target, the system monitors whether the price comes back to the entry level:

Re-Entry Types

You can configure how the re-entry condition is checked:

Examples

Example 1: Option Target with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option Target with LTP Basis (Buy Entry)

Flow:

Example 3: Underlying Target with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying Target with LTP Basis (Call Buy Entry)

Flow:

Other Configurable Parameters

Stop Re-Entry Time

Number of Re-Entries

W&T with Re-Entry @ Cost

Note:

The following options are not applicable for Target-based Re-Entry:

The Re-Execute on Target feature allows the system to open a new position after the target is achieved. Unlike Re-Entry @ Cost, which waits for the price to return to the original entry price, Re-Execute triggers a fresh entry directly after the target is hit, based on user configuration.

In Re-Execute on Target, the system always selects a new contract as per the active contract selection method when re-execute triggers.

How Re-Execute Works

After the target is hit:

Re-Execute Types

Examples

Example 1: Option Target with Candle Closing Basis (Sell Entry)

Flow:

Example 2: Option Target with Immediate Re-Execute (Buy Entry)

Flow:

Example 3: Underlying Target with Candle Closing Basis (Call Sell Entry)

Flow:

Example 4: Underlying Target with Immediate Re-Execute (Call Buy Entry)

Flow:

Key Differences Between Re-Entry @ Cost and Re-Execute on Target

| Feature | Re-Entry @ Cost | Re-Execute on Target |

| Entry Condition | Waits for price to return to original entry price | Triggers after target hit based on immediate or candle close setting |

| Contract Selection | Same contract as original | New contract selected as per contract selection method |

| Timing | LTP basis or Candle Closing basis | Immediate or Candle Closing basis |

The Re-Execute Reverse for Target feature works similarly to Re-Execute on Target, but with one key difference:

It alternates the direction of each re-execute after a target is hit.

How Re-Execute Reverse Works

Behavior Summary

| Target Hit Count | Action Type (for initial Sell entry) |

| 1st Entry | Sell |

| After 1st Target | Buy |

| After 2nd Target | Sell |

| After 3rd Target | Buy |

| And so on… | Alternates each time |

Hedge contracts can be configured for each strategy leg to reduce margin requirements or manage risk exposure. You can select the hedge contract in two ways:

In both methods, separate configuration is provided specifically for hedge contract selection, allowing independent control over how hedge contracts are chosen.

Additionally, there is a special option:

During exit, the system always exits the main leg first, and once completed, it exits the hedge leg.

Method 1: ATM Points Based Hedge Selection

This method selects the hedge contract based on its distance from the ATM strike in terms of strike steps.

How it works:

Example:

Note:

Method 2: Closest Premium Based Hedge Selection

This method selects the hedge contract whose premium is closest to your specified target premium using configurable match conditions.

How it works:

You need to specify:

Example:

Premium Match Options:

If no contract is found within the specified match range, you can configure the fallback behavior:

Note:

Hedge premium match uses a separate Hedge Match Settings section.

You can configure it with two options:

Example:

Example:

Parameters

Example:

Flow:

Note:

The Combined SL feature allows you to define a stoploss at the portfolio level based on the combined entry price of multiple legs.

Prerequisites:

How Combined SL Works:

Example:

Available Parameters for Combined SL:

Trailing SL: X and Y configurable in % or Points

Note:

Other advanced re-entry filters (Wait for Original SL, Disable Re-entry if SL moved to cost, etc.) are not applicable for Combined SL Re-Entry.

Re-Execute Types:

Configurable Parameters:

Stop Re-Execute Time

| Combined SL Hit Count | Entry Direction (assuming initial Sell) |

| 1st Entry | Sell |

| After 1st SL | Buy |

| After 2nd SL | Sell |

| After 3rd SL | Buy |

| … | Alternates each time |

The Combined Target feature allows you to define a target at the portfolio level based on the combined entry price of multiple legs.

Prerequisites:

How Combined Target Works:

Example:

Available Parameters for Combined Target:

Note:

Other advanced re-entry filters (Wait for Original SL, Disable Re-entry if SL moved to cost, etc.) are not applicable for Combined Target Re-Entry.

Re-Execute Types:

Configurable Parameters:

Candle timeframe

Stop Re-Execute Time

| Combined Target Hit Count | Entry Direction (assuming initial Sell) |

| 1st Entry | Sell |

| After 1st Target | Buy |

| After 2nd Target | Sell |

| After 3rd Target | Buy |

| … | Alternates each time |

Order Settings allow you to control how orders are placed and managed for:

You can configure different settings for Entry Orders and Exit Orders independently.

Order Type

You can select:

Limit Price Configuration (Applicable for Limit Orders Only)

Limit Price Calculation Examples

Example 1 — LTP Reference

Example 2 — BestBidAsk Reference

Example 3 — ImFill Reference

Example 4 — AvgBidAsk Reference

Limit Order Revision Logic

If the limit order is not filled, the system can automatically modify it using the following two revision methods:

Option 1: Modify to Market

Option 2: Revise Limit Price

Separate settings apply for orders placed as Stoploss (SL) orders in broker.

Order Type for SL Orders

Trigger Price

Limit Price for SL Order

Limit Price Calculation Example

(For Buy orders, buffer is added to Trigger Price; for Sell orders, buffer is subtracted.)

SL Order Revision Logic (Same as Entry/Exit orders)

📸 [Screenshot showing SL Order Settings with Limit Buffer and Revision Logic]

Summary

| Configuration | Entry Orders | Exit Orders (Non-SL) | SL Orders |

| Market Order | Available | Available | Not Available |

| Limit Order | Available | Available | Always Limit |

| Limit Reference | Available | Available | Available |

| Limit Buffer | Available | Available | Available |

| Revision Logic | Available | Available | Available |

Max Loss defines the maximum allowed drawdown.

Example (Strategy Level):

For Account Level / Global Level:

Parameters for Max Loss:

Ticks Based:

Exit only if Max Loss condition holds true for X number of consecutive ticks.

Trail Max Loss allows you to dynamically tighten your Max Loss as profit increases.

Parameters:

Example:

Flow:

Same behavior applies for Account Level and Global Level — only MTM calculation changes as per level.

Max Profit defines the maximum profit at which you want to exit and book profits.

Parameters and behavior are exactly same as Max Loss:

Frequency to Check, Exit Mode, and Ticks Based logic all apply exactly as in Max Loss.

Protect Profit helps secure profits dynamically as your profit grows. Three modes are available:

Allows you to lock a fixed minimum profit once your profit crosses a threshold.

Parameters:

Example:

Flow:

Allows you to trail profits upward step-by-step as profits grow.

Parameters:

Example:

Flow:

Combines both Lock and Trail methods together.

Parameters:

Example:

Flow:

Applicable Behavior Across All Levels:

| Level | MTM Calculation |

| Strategy Level | MTM of individual strategy |

| Account Level | Total MTM across all strategies of that account |

| Global Level | Total MTM across all accounts |

Deepak Chandan –

Super speed good platform for algo

Apricus Consulting pvt Ltd (verified owner) –

Excellent 👌

Vikas gupta –

I have been using this option trading software for some time, and I find it very helpful. The best thing is that it is simple and easy to use. Execution is smooth and quick, which makes trading stress-free. The software runs without any problems and provides real-time updates, which is very useful for option trading.

I also like that the platform is stable and reliable. It saves a lot of time and effort by making the whole process straightforward. With this software, I can focus more on my trades instead of worrying about technical issues.

Another great point is the excellent customer support. The best part of the software is Dharmesh bhai, who is always available for help and guidance whenever needed. His quick response and support make the overall experience even better.

Overall, this software has made my trading journey much easier and more comfortable. I would definitely recommend it to anyone looking for a simple, reliable, and trustworthy option trading software.

macchap (verified owner) –

Simply the best algo trading software if you are doing intraday straddles and strangles. One can configure all the parameters that is required for various different types of strategies. I have been using this for nearly 2.5 years and whenever I wanted support, they have provided the required resolution promptly.

Siddhartha Timbadia (verified owner) –

Your software is best and fast for exiting trade at stoploss to keep traders on safe side.

Not got any technical issue till now with easy to use features.

Best algo software so far …

Moreover, Dharmesh Sir is so supportive and helpfull in everyway.

I am not getting this at other companies like stoxxo.

Keep growing and thank you

🙏🏻